In other words, when the spectre of an independent Scotland was not dangling over their heads. But now that spectre – originally touted as a once-in-a-generation occurence – is hovering once more. Emboldened by the closeness of the referendum result the SNP is suggesting independence is once more on the table, but refuses to be drawn on when. As EG went to press the SNP Manifesto, which might be expected to shed some light on the matter, had still not appeared. Of course, to call another referendum, the SNP would need to be in charge of the Scottish Parliament, but with the next election less than six months away in May 2016, few are predicting anything other than an SNP landslide, unless a Corbyn-catalysed Labour Party makes an eleventh hour comeback.

In other words, when the spectre of an independent Scotland was not dangling over their heads. But now that spectre – originally touted as a once-in-a-generation occurence – is hovering once more. Emboldened by the closeness of the referendum result the SNP is suggesting independence is once more on the table, but refuses to be drawn on when. As EG went to press the SNP Manifesto, which might be expected to shed some light on the matter, had still not appeared. Of course, to call another referendum, the SNP would need to be in charge of the Scottish Parliament, but with the next election less than six months away in May 2016, few are predicting anything other than an SNP landslide, unless a Corbyn-catalysed Labour Party makes an eleventh hour comeback.

For now, then, the assumption is that an SNP-controlled Scottish government will continue to rule the roost. What effect will that, and the undefined promise of another referendum, have on those considering investing in Scottish property? Depending on who you speak to, the answer varies from “not much” to “quite a bit”. John Bingham, head of real estate at Glasgow-based legal firm Bellwether Green, speaks for many in the industry when he says: “Independence is not financially viable – it just doesn’t work. The ultimate message is that the numbers tell the story.” That may well be true (see box), but the No campaign struggled during the referendum run-up to make the numbers accessible.

There are also demographic reasons why a future vote will be equally unsuccessful, points out Bruce Patrick, Savills’ Glasgow-based director of UK investment, but could the threat of it still push potential investors away? Unlikely, according to Patrick: “The attitude on the ground is that the ‘Neverendum,’ like Brexit, is pretty much background noise. Investors are attracted by returns – the risk is factored into the yield.”

Scottish prime yields are 50-100bps below similar products in England. “There has always tended to be a differential,” notes David Stewart, property fund manager at Standard Life Investments, “but if there is rental growth, which I would expect, they may come in slightly.”

Not everyone believes the outlook ahead of next year’s election is rosy.

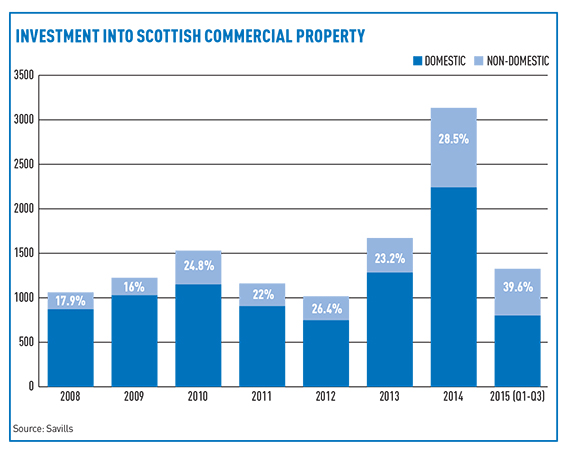

“We are seeing a slowdown already. This should be the busiest time of the year,” observes Mitchell. Foreign investment, which has grown significantly recently (see graphic) and is more resilient to local politics, could account for more sales next year, although Bilfinger GVA senior director Stuart Agnew warns: “The lack of stock of sufficient scale may be an issue for the wave of new Asian and North American money that is likely to have a significant impact on trading in 2016.”

PRS (see below) could also bring in new investment.

“I am quite convinced it will happen, although we have only recently got to the place where the mindset of developers and investors has changed,” says Ramsay Duff, investment director of Maven Capital Partners. The key message to prospective buyers, concludes Bellwether Green’s Bingham, is: “You are right to be scared about an independent Scotland, but the economic case is so flawed it is never going to happen.”

Do the numbers add up for an independent Scotland?

Earlier this year respected economist Professor Brian Ashcroft, now retired as director of the Fraser of Allander Institute – an independent Scottish regional economic research unit – rounded on the Scottish government for publishing the results of economic modelling which produced: “political-economy outcomes that are fanciful and are lacking in economic rigour.” Ouch.

Earlier this year respected economist Professor Brian Ashcroft, now retired as director of the Fraser of Allander Institute – an independent Scottish regional economic research unit – rounded on the Scottish government for publishing the results of economic modelling which produced: “political-economy outcomes that are fanciful and are lacking in economic rigour.” Ouch.

What really raised Ashcroft’s ire was what he believed to be an implicit calculation by government economists that an independent Scotland would be able to retain UK subsidy (the Barnett formula) as well as full tax revenues, something he describes as “totally unrealistic”.

Ashcroft’s detailed analysis of the true cost of Scottish independence on his Scottish Economy Watch blog make for interesting reading, but demonstrate the challenges faced by unionists during last year’s referendum campaign in distilling complex data into an easily accessible format. Ashcroft, who points out that his views are independent, is seen by many Scottish property players as putting forward reliable and cogent arguments that undermine Scottish government assertions about the viability of an independent Scotland.

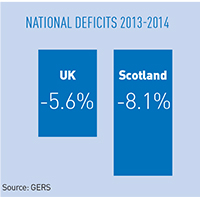

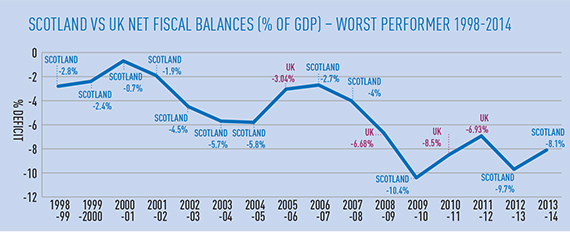

Picking through the latest official economic data (which relates to 2013-2014) in March Ashcroft observed that Scotland’s deficit was higher than that of the UK, meaning that if Scotland had been independent in that year it would have needed to find an additional £3.8bn of funding – a considerable amount (half the cost of the country’s education and training budget, for example). Importantly, Ashcroft showed that historically Scotland’s deficit has been greater most years since 1998. “What that means,” he commented, “is that in 12 of the 16 years, if Scotland had ‘enjoyed’ full fiscal autonomy it would have had to have higher taxes, lower public spending or both than the UK.” (see graphic below)

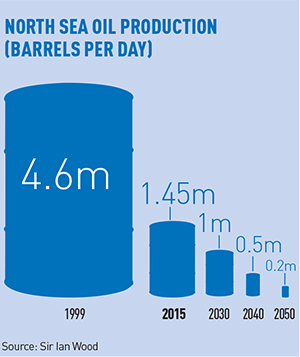

Ashcroft also pointed out that North Sea oil and gas revenues are on a declining timeline (see next page) and in the meantime are very unpredictable, calling into question how much they would actually contribute to the economy of an independent Scotland. The Scottish government has made assumptions based on Brent crude prices of $110 (£72.30) per barrel – yet at the beginning of this month, according to the US Energy Information Administration, they were dropping towards $47 per barrel.

When will the oil run out?

The death of the North Sea oil and gas industry has been predicted for a long time, yet oil companies have defiantly continued extracting energy. However, most parties agree that the supply is finite and oil production has fallen pretty much continuously since 1999. So for how much longer will oil continue to flow from the North Sea? This is a crucial question for an independent Scotland.

The death of the North Sea oil and gas industry has been predicted for a long time, yet oil companies have defiantly continued extracting energy. However, most parties agree that the supply is finite and oil production has fallen pretty much continuously since 1999. So for how much longer will oil continue to flow from the North Sea? This is a crucial question for an independent Scotland.

In September retired oilman and billionaire Sir Ian Wood gave his view to Scottish media (see graphic, left), which suggests production will be down to 15% of its current level by 2050 and the effects of this would be felt considerably before then.

He commented: “The practical impact is that, probably no later than 2030, we will begin to see surplus capacity in hotels, pubs, restaurants, retail outlets, rented properties, housing and many other sectors.”

Two steps backward, one forward for PRS

The chatter among investment specialists in Edinburgh and Glasgow is whether PRS will ever make it to Scotland. David Mitchell, managing partner of Scottish property company Manse, frames the question doing the rounds: “At a time when the UK is trying to increase the supply of residential stock why is the Scottish government creating barriers and uncertainty?” Mitchell is referring to the proposed Private Housing (Tenancies) Bill, a draft of which finally appeared last month.

Until then there had been huge concern that the Bill, designed, according to the politicians, to protect tenants against the threat of eviction and big rent increases, could effectively stymie rental growth, making PRS investment north of the border a serious no-no. Now at least the cloud of uncertainty has been lifted. “It has removed a psychological block for investors looking at PRS in Scotland,” confirms Mark Donnelly, corporate recovery associate director at Colliers International. He concedes: “It is not as attractive as purely market-driven rents as in London or other regional markets, but it removes the absolute doubt that investors should invest in PRS here.”

Author: Mark Simmons

Link: http://www.egi.co.uk/news/scotland-investment-a-curious-case/?keyword=manse